Ratio charts are one of my favorite things about technical analysis. They allow us to compare how a particular security is performing relative to its benchmark or another security. As trend followers, we expect current market trends to continue until sizeable evidence is introduced that proves otherwise. Ratio or relative strength charts help us identify and confirm these trends. We’re not here to proclaim the market is wrong or place large bets on a potential mean reverting price move (Try it and let me know how it goes). We’d much rather identify well-founded trends in the market and participate in them as best we can. This opens the door for scalable risk management practices and allows us to remain invested in the strongest industries within the strongest sectors of the market. It all starts and ends with relative strength, baby!

Let’s take a look at the US Smallcap Sectors and how they are faring relative to the S&P Smallcap 600 Index. To begin, we’ll take a look at Energy. This sector is up +38% year-to-date, but the relative strength chart remains in neutral territory. The June ‘20 peak remains our line in the sand. If the ratio trades above it, it may constitute a legitimate change in trend. The 14-period RSI remains neutral as well, having hit oversold in October and overbought in November.

Next up is Materials. The Smallcap sector had a very strong finish to 2020, but to start the new year has witnessed a big decline in its relative strength chart. It appears 0.75 is behaving as a significant zone, the ratio has not traded above it since April ‘18. Any break above that zone would be extremely notable.

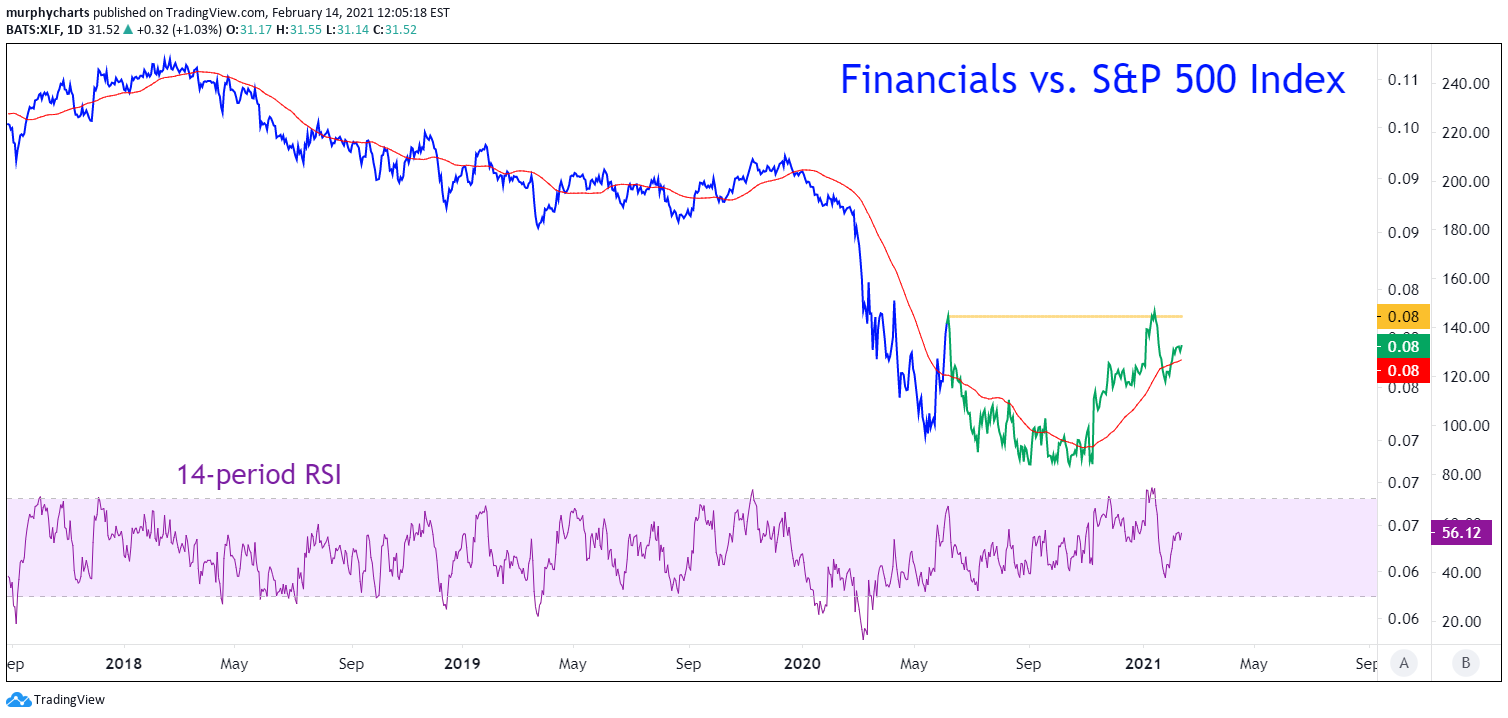

Now we have Financials. It’s important to note that this Smallcap Sector ETF consists of both Financials and Real Estate stocks. Any thesis built around Smallcap Financials must take this into consideration, as Real Estate remains a lagging sector across all market cap sizes. With that being said, the ratio reached a new low this January.

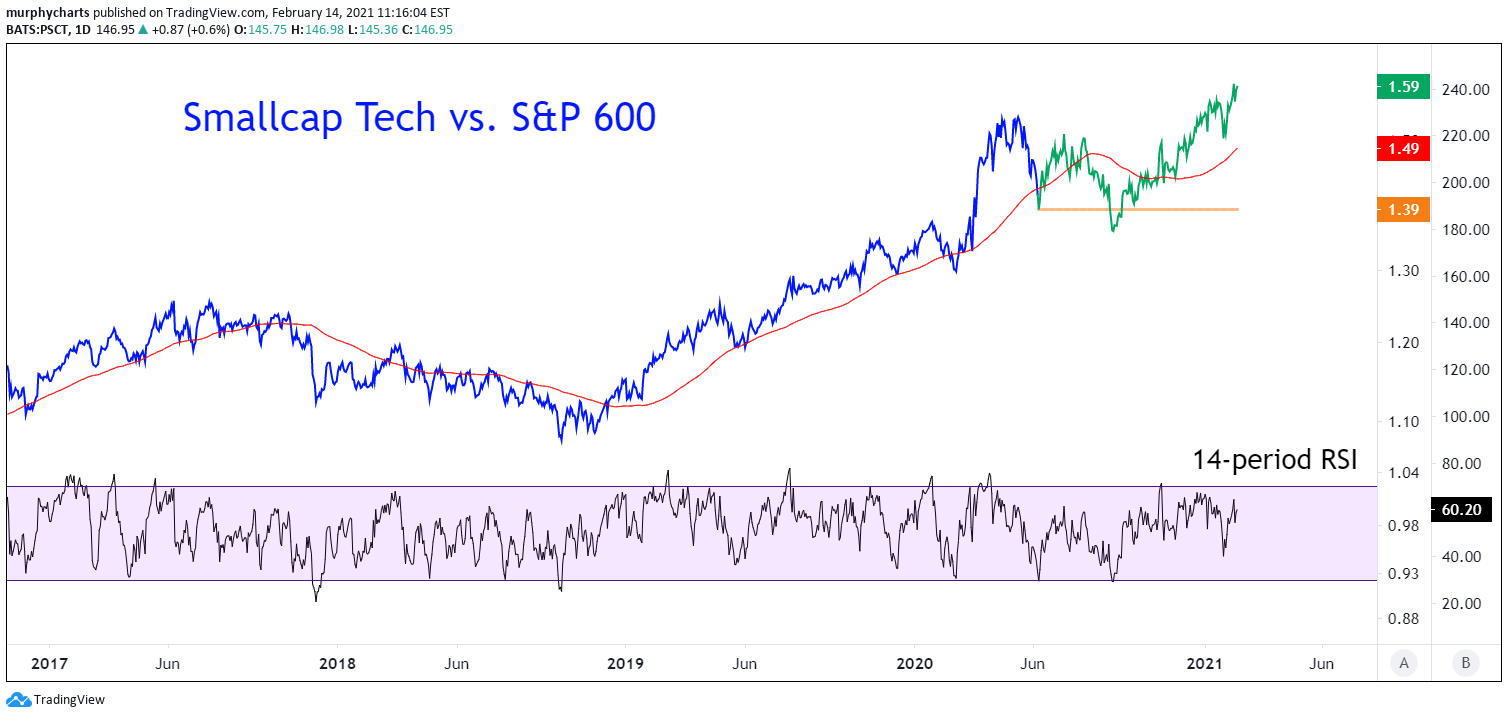

The last Smallcap Sector I’d like to bring to your attention is Technology. The relative strength chart reached another new all-time high this month. Although Largecap Tech is yet to surpass its 52-week relative high (printed in September ‘20), Smallcap Tech is making new all-time highs on both an absolute and relative basis in 2021.

Okay, that’s enough of the Smallcaps. How about the big guys relative to the S&P 500 Index? First up, the most talked about sector in recent months. Financials. With the yield curve gradually steepening, and the US10Y climbing higher, the tailwinds hitting the back of the Financials sector are enough to have any investor interested. However, the relative strength chart is struggling to break above its June ‘20 high. Just like we discussed with Energy, a move above this area may constitute a legitimate change in trend. Only time will tell. It is notable that Regional Banks on a relative basis are above their June high, but this is primarily due to the industry consisting of Smallcap & Midcap stocks.

Next up is my favorite US Sector. Healthcare. In my opinion it is the most diverse sector in the market. The relative strength chart is beginning to pique my interest. The 14-period RSI is diverging from price, this is notable - however until we see price confirm the divergence and resolve higher, that is all it is. Notable. The ratio peaked in April ‘20 and has been in a downward trend ever since. I’ll be keeping my eyes on this one for sure. From a valuation standpoint, pharmaceutical stocks are trading at a discount relative to the broad market i.e. BMY, MRK, PFE are all trading below the S&P 500’s NTM Price to Earnings ratio. This is a valid data point in my opinion.

Right now stocks are trending higher with an increased level of risk appetite. Below is a chart of the Semiconductor industry relative to the S&P 500 index. This industry has been trending higher on a relative basis for over 1.5 years. Just last week the ratio made another new 52week high.

Both the Utilities and Consumer Staples sector reached new relative lows this week. The two most defensive US Sectors are reaching new relative lows, while more risk-on areas of the market are making new highs. This is what happens within an equity bull market. Whether or not the new cyclical bull lasts 6 months or 3 years is beside the point. Manage your risk and search for strength!

That’s enough outta me!

SM

Awesome write up