If you are a twenty-something adult in the US, there’s a good chance your liquidity needs are very high. You’re either saving for your first home, car, looming education expenses, an engagement ring or a number of other things. If you’re lucky, you’ve developed a savings bucket that is earmarked for the experiences that make up your “life portfolio” i.e. travel or vacations. You cannot afford to have your non-retirement savings be invested in risk assets. If we see a 20% decline in equities and you need to withdraw funds for a down payment - you are shit out of luck, my friend.

So what’s the solution?

Is there a special product out there that can earn 2-3% but also avoid risk and offer high liquidity? No. If that changes, I’ll let you know - but don’t count on it!

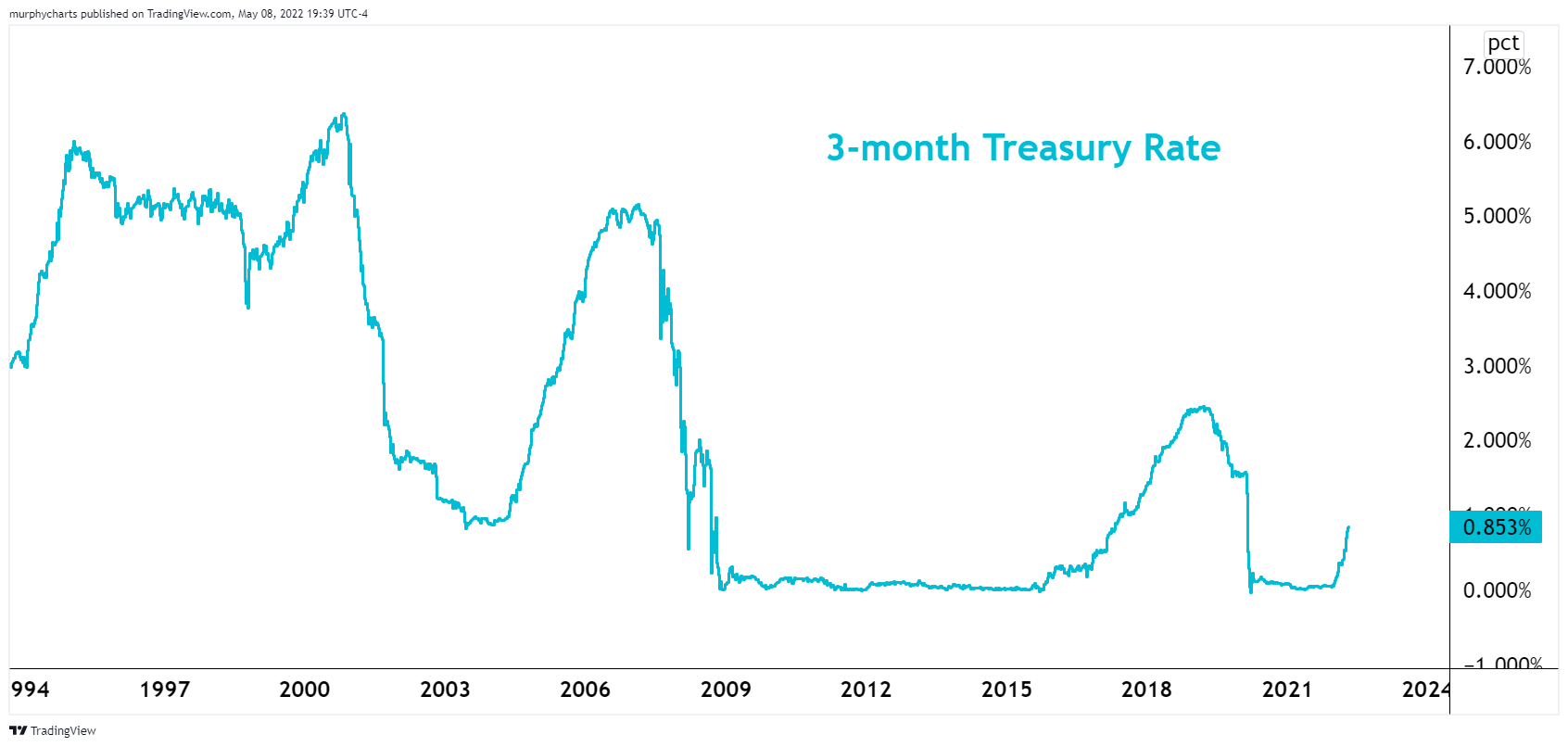

Cash is cash for a reason, it is called the risk-free rate for a reason. The 3-month Treasury Bill Rate is at 0.853%. If you want sizeable returns, you will be required to take on risk.

The phrase “Reward-Free Risk” comes to mind when evaluating some of the higher earning money market funds available to investors. Remember, money-market funds are not FDIC insured, unlike your bank savings account or money-market deposit account (MMDA).

Okay, I’ll get to the point.

The point is, we must be accepting of low interest rates in our bank savings accounts. In my opinion, attempting to finesse a few hundred basis points of yield by taking on risk is a poor decision. Especially if these funds are earmarked for important life events.

Explore high-yield savings accounts, ask your bank/credit union if a higher tier is available. Do what you can, but don’t get caught up in trying to earn more on your savings bucket. It is serving its purpose. It was suggested to me to focus less on yield, and more on becoming aware of each bucket’s time horizon. I think that makes a lot of sense! The more we home in on each bucket’s function and expected timeline, the better we can maximize the use of our future capital i.e. allocate more into risk assets or become more accepting of volatility in our investment accounts. Maintaining liquid, low-to-no risk assets is an important part of any investor’s arsenal. It’s not just the stock portfolio that we need to spend time thinking about!

That’s enough out of me.

SM

Great article that people should pay attention to